Signaling that hard market conditions may be easing, commercial insurance rates in the U.S. are still increasing but at a slower rate, according to several recent reports.

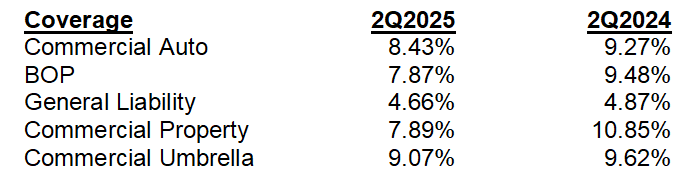

The most recent IVANS INDEXTM showed rates increasing at a slower pace in the second quarter of 2025 for all major commercial lines of coverage other than Workers’ Compensation. The most distressed line, commercial auto, climbed 8.43%, but that was down from 9.24% in the first quarter. Business owners, commercial property, and commercial umbrella saw similar decelerations in the rate increases, while commercial general liability actually rose at a faster pace, increasing 4.66% versus 3.95% in the first quarter.

The increases were generally also below 2024 levels:

Workers’ Compensation rates continued to decrease and at a faster rate. The second quarter decrease was 1.75% as opposed to 1.51% in the first quarter and only 1.29% in the second quarter of 2024.

These patterns were not uniform. For example, while the countrywide increase for commercial auto was 8.43%, Florida saw double-digit increases. Similarly, double-digit increases were reported for BOP in Mississippi and General Liability in Alaska.

Travis Schenck, marketing strategist for Arizona-based agency network Dark Horse Insurance Brokers, said the experience of agencies in that network bear this out. Noting that commercial and personal rate increases are on average below 10%, he described rates as “stabilizing and even in some cases beginning to decrease.” However, the decreases appear to be carrier driven rather than across the board for a given line of coverage: “The insurance companies that took early action on rates are ahead of the game, while some of the late adopters are still seeing rather substantial increases.”

Other reports show the same trend. The MarketScout Market Barometer showed a slowing of rate increases in the quarter. Hub International made a similar report, but cautioned that conditions remain tight for some lines and in some parts of the country. Regarding commercial auto, “Carriers have required more detailed submissions that include zip-code level data and at least 10 years of loss histories to assess and price risks,” the report said.

Commercial property rate increases vary by program structure and area of the country, Hub said. Shared and layered programs are experiencing stable rates, while single-carrier placements are subject to higher increases and underwriting scrutiny, particularly in high-risk areas such as California.

Hub also had words of caution regarding the Workers’ Compensation market. “Select carriers are pursuing modest increases driven by profitability concerns,” they said. “Economic pressure and potential shifts in employment patterns could further elevate claim frequency heading into late 2025.”

The U.S. is an outlier compared to the rest of the world, according to Marsh’s Global Insurance Market Index. Global insurance rates declined for the fourth consecutive quarter in the second three months of 2025, with rates down an average of 4%. “Declines were experienced in most regions and product lines,” March reported, but, “The composite rate declined in all regions except in the US, where the rate was flat.” The Marsh survey may have included product lines that the IVANS index did not, such as cyber and professional lines.

What comes next? Schenck said, “All of the feedback that we have received from our insurance company partners is that Q3 of 2025 is the transition point for most, and 2026 will be working towards getting back to business as usual.” The accuracy of that prediction may hinge on catastrophes in the second half of the year. To date the Atlantic hurricane season has been quiet. If it remains that way, the market may be on the road to more stabilization next year.